According to the Garnaut Report, Australia leads the OECD in per capita carbon emissions. Why? Well, the Australian government has pegged the energy industry as being responsible for three-quarters of our carbon emissions.

In fact, the National Greenhouse Gas Inventory reckons total emissions from the Australian electricity sector was 193 million tonnes in year ending March 2012. Although there are reports that this level is dropping slightly, that's still a lot of carbon dioxide--equivalent to more than seven billion home BBQs.

Figure 1. Net CO2-e emissions in by the energy sector in Australia.

Source: Department of Climate Change and Energy Efficiency

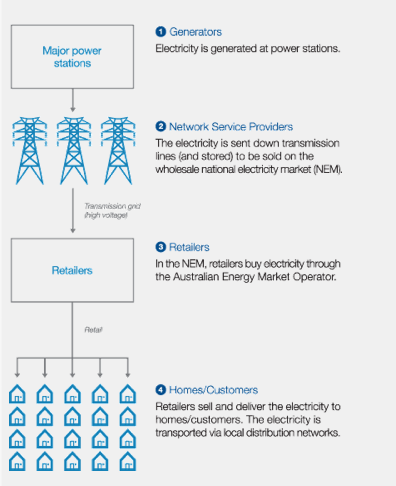

A fractured industry: four components and countless regulations

The industry is not simple to understand. There are different fuel types—coal, gas, wind, water, sun. And prices, contracts and regulations vary from state to state. To make matters more complicated, the industry is sub-divided into four components: generation, transmission, distribution and retail.

Figure 2. Graphic depicting how electricity works in Australia.

Source: CS Energy

The best way to explain the impact electricity has on carbon emissions is to go step by step (generation, distribution/transmission and retail) and consider the impact that the current system has on carbon emissions.

Generation: Green plants don’t always stem from green parents

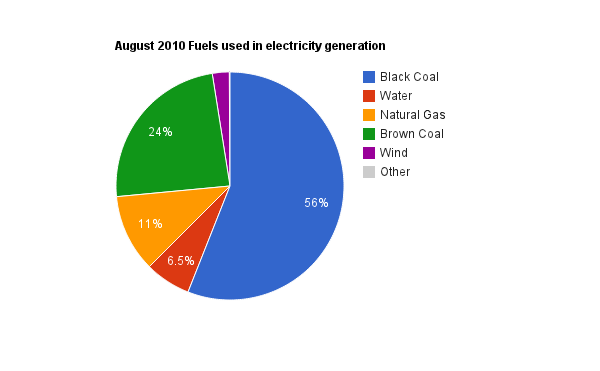

Electricity is generated in hundred of plants across Australia (322 in the NEM alone, plus independent operations such as the mines in the NT and WA). As our reliance on brown and black coal wanes, renewable energy (especially wind and water) occupy a bigger piece of the NEM than they did even two years ago. So it seems a fait accompli: less coal, more green power equals fewer emissions.

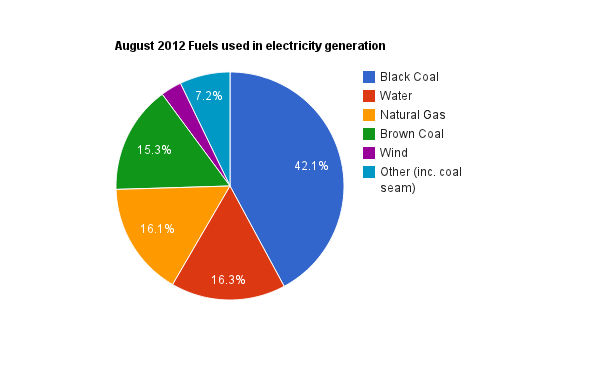

Figure 3. Comparing fuels used for electricity generation in the NEM, August 2010 and August 2012

Source: New Matilda analysis of Australian Energy Market Operator (2012) and Garnaut Report (2010) data

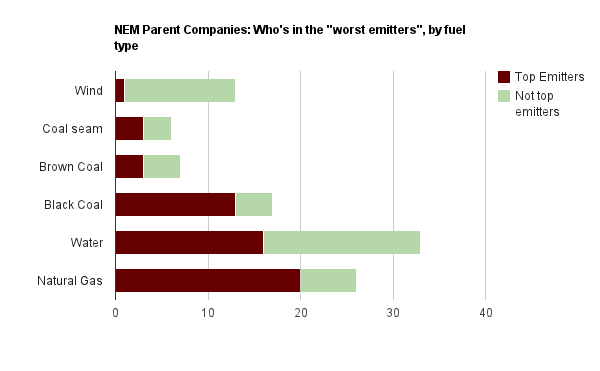

But dig a bit deeper. Who are the parent companies funding each generation plant? And how green are they? New Matilda looked at ratio of ‘emitting’ to ‘clean’ parent companies. Natural gas doesn’t look so clean (3.3 emitters for every clean company). Wind had a high number of clean parent companies, but water had a surprising number of top emitters.

Figure 4. NEM Parent Companies: Worst emitters by fuel type

Souce: New Matilda analysis on top emitting companies published by Clean Energy Regular-National Greenhouse and Energy Reporting

In other words, having one or two clean generation mechanisms does NOT equal a carbon-friendly parent company.

Remember that these ratios are based on the NEM, which excludes all of the mines in the NT and WA. Here’s food for thought: the electricity used to power the mines in the NT is emitting more carbon than the electricity powering the city of Darwin. Barry Brook estimates that the greenhouse gas emissions from the Olympic Dam mine expansion would lead to an additional 4.7 million tonnes/year, equivalent to the electricity use of half a million homes.

The mining industry is not too excited to invest in greener generation: why invest in technology that takes a decade to recover costs when your operation shuts after three years? Here’s a direct quote from the annual report of Hamersley iron, which a $225 million annual royalty payment to Gina Rinehart:

“To reduce the production of greenhouse gases further the proponent has considered the option of installing a combined cycle power station at an additional cost of $320M. ... However, because of the high up-front cost of this option, combined cycle power generation is not considered economic and will not, therefore, be adopted.”

Generation Next: Getting Picked for the Team

After the electricity is generated in a plant, generators sell their electricity into a pool and retailers buy electricity from the pool. In the eastern states, pooling the generated power is centralised as the NEM collects electricity under the management of the Australian Energy Market Operator (AEMO).

How does this pooling work? Imagine the selection process for a school yard footy team. All lined up, the generators bid to supply electricity into the pool. “Pick me, pick me.” Starting with the cheapest offer, bids are selected. Selection stops when the NEM has enough power to meet demand. Don’t be too disheartened if you weren’t picked; the next round starts in five minutes.

Now here’s the part that drives prices: the dispatch price for each five-minute interval equals the bid of the last player selected. And the wholesale price is the average of these bids over a half-hour. Now, the leaner, fitter greens are crowding the field (wind farms even offer negative bids because that’s cheaper than shutting off their supply). Larger, chunky coal is being overlooked: wholesale prices are dropping and these kids-who-once-were-kings are left sulking on the sidelines. They just can’t keep up.

Source: Wind Energy - Penetration and Spot Revenue by Stephen Weston and Yannick Godin

What’s critical here is that there is only one factor--price--determining team selection. That leaves no room to assess the carbon emissions of the players. Laissez-faire economists contend this myopic fixation leads to survival of the fittest. Or are we simply choosing the dregs from a yard full of asthmatics?

Transmission and Distribution

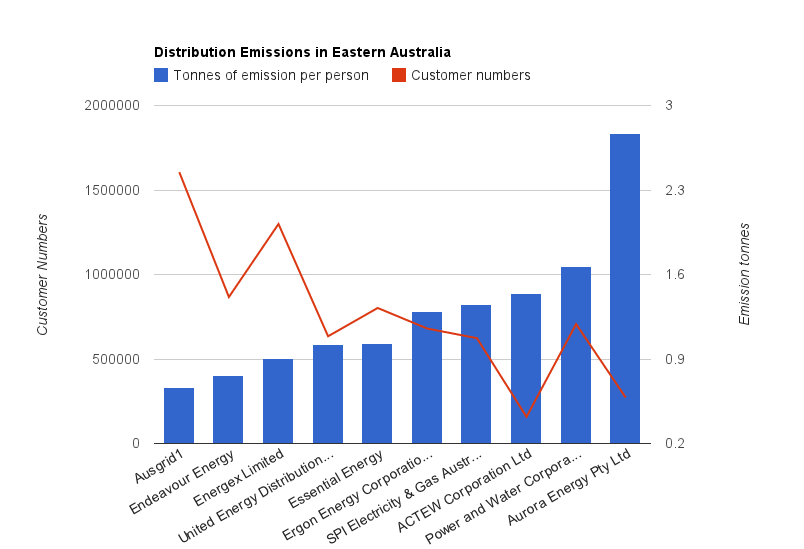

Next in the process comes distribution and transmission--the “poles and wires.” Again, before the carbon legislation, these businesses had little reason to invest in eco-friendly infrastructure. Take the following chart--New Matilda found that ACTEW and Aurora Energy serve about the same number of customers, yet Aurora has nearly double the CO2 emissions per customer. Still, economics --and geographic monopolies--are the only factors in determining which transmission/distribution company gets to carry the team.

Figure 6. Emissions of the Distribution Networks (by company and customer numbers) in Eastern Australia

Source: New Matilda analysis of NGERS data

The systems are different outside the NEM. In WA’s South West Interconnected System, electricity is traded directly between generators and retailers. At the other extreme, one government utility in the NT is responsible for generation, transmission and retail. Indeed, the NT government wants to focus on greener solutions. But its hands are tied by vast distances--there are still countless independent operators.

It can only encourage the independent generators and distributors to move from diesel to solar. Remote aboriginal communities are helping the NT meet its goal of eliminating diesel, mines are dragging their feet.

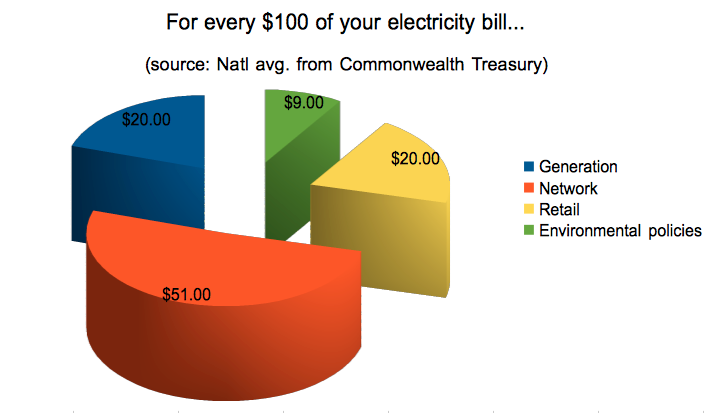

Figure 7. Breakdown of electricity costs by component

Source: National Average from Commonwealth Treasury in cleanenergyfuture.gov.au

Retail

Electricity retailers are those businesses that sell electricity directly to the general public.

Think of them as the talent scouts. Across Australia, more than 33 retailers watch the game, pick what they like, and pass it onto the public. The Garnuat Review notes that retail relationships in the NEM are opaque. Retailers contract for supply in the event of high demand and thereby avoid the impact of high spot prices. Critically, there is no established mechanism to deal with contract market instability. Deals are made and players are swapped; the talent scouts come out on top while resting unassumingly at the bottom of Australia’s electricity totem pole.

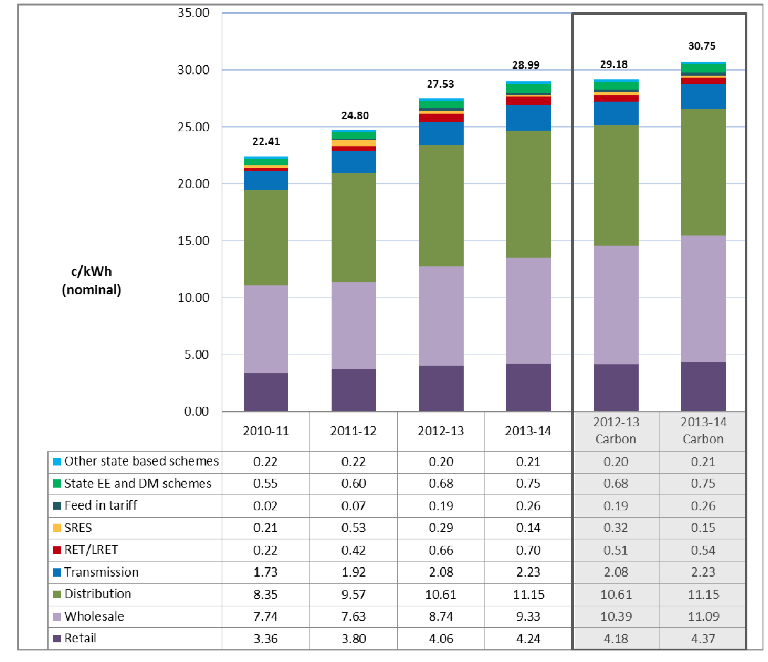

Figure 8: Summary of current and future possible residential electricity prices in Australia from 2010/11 to 2013/14

Source: Australian Energy Market Commission

This is a competitive industry, and retailers are being held accountable to the Renewable Energy Target (RET). The goal of the RET is to ensure 20% of electricity generated in Australia is from renewable sources in 2020. Under the scheme, a certificate can be created for each megawatt-hour of renewable generation produced. Electricity retailers must purchase a target number of certificates each year; RET means they must choose the lean and green for their team.

But the RET and its accompanying Renewable Energy Certificates (REC) aren’t all sunshine. As part of the 2009 economic stimulus, the government quintupled the REC multiplier for domestic hot water and solar. In other words, generally one REC represents one megawatt hour of electricity produced by a renewable source, but under the new policy solar and hot water were allowed steroids while wind was left to its own devices. This move destroyed the entire wind industry for the past three years; wind is still blown over by the overhang of these so-called "phantom RECs".

Equally dead is Christine Milne’s 2010 amendment to the Renewable Energy (Electricity) Act 2000 required that the number of renewable energy certificates (RECs) created by solar hot water systems, heat pump hot water systems and ‘phantom RECs’ to be added to the subsequent year’s renewable energy target. The continued influence of retailers’ phantom RECs mean that the renewable energy target is further away.

Conclusion

At first glance, the electricity sector is moving in the right direction. The playing field is level with more green power; dispatch prices and carbon emissions are lowering, albeit slowly. But even with some green effort, the major parent companies are still suspect--especially in the areas of transmission and distribution. The Garnaut report calls for tighter regulation, but there is little incentive to reduce wasted electricity or carbon emissions along the poles and wires.

(Note: I am interning at New Matilda.This is the first version of an article I am co-authoring with Ben Eltham. If you're reading this, you should also read the final (really comprehensive--go Ben!) articles on the New Matilda website: "Your Energy Bill Explained" and "Poles, Wires, Regulator and Middle Men".)

No comments:

Post a Comment